Share prices of Salesforce (NYSE: CRM) plunged last week after the company released its latest quarterly results. While the business is still growing, it didn’t provide analysts and investors with the level of growth they were expecting. For a stock that trades at a relatively high valuation, that could put it in a dangerous position.

Salesforce is still a dominant name in the tech world, and its customer relationship management (CRM) platform fulfills crucial needs for many businesses. But there are clearly some issues it’s going through.

Should investors consider buying the tech stock after its recent pullback to take advantage of what might just be a short-term issue? Or does Salesforce have bigger problems on its hands and now’s the time to get out or avoid buying?

What went wrong for Salesforce?

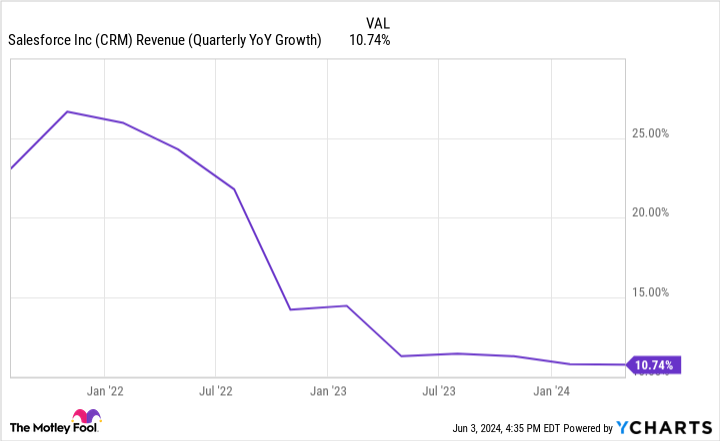

Salesforce stock had its worst day in decades after posting its first-quarter numbers in the last week of May. What was particularly noteworthy was that the business fell short of analyst expectations for the first time since 2006. Salesforce has typically satisfied investors and analysts with its results, but not this time.

For the first quarter of fiscal 2025, which ended on April 30, the company’s revenue totaled $9.13 billion and rose by 11% year over year. But analysts were expecting $9.17 billion in revenue. Furthermore, the company’s forecast for the current quarter was also underwhelming, with management projecting a range between $9.20 billion and $9.25 billion in revenue. Analysts were expecting as much as $9.37 billion in sales.

Expectations are high for an expensive stock

Salesforce has enhanced its CRM platform with artificial intelligence (AI), which it calls Salesforce Einstein. Einstein can help anticipate sales opportunities, proactively resolve cases, and “embed intelligence everywhere.” The company brands its platform as “the #1 AI CRM” and says that it’s “well positioned to help companies realize the promise of AI over the next decade.”

The problem with those kinds of claims is that if you want to convince investors that you have new AI-powered products, then there should be some evidence of that in the way of a higher growth rate. But that isn’t the case. In fact, Salesforce’s growth rate has been slowing down for several quarters.

That’s not the type of growth I would expect from a company that’s hyping up its AI-related growth opportunities.

Salesforce’s valuation remains high

Salesforce’s stock trades at more than 40 times its trailing earnings. And that’s after factoring in last week’s sell-off. It’s a high valuation for a business that is expecting just single-digit growth for the current quarter, between 7% and 8%.

At a high earnings multiple, investors are going to be expecting much better results than what Salesforce delivered in its most recent quarter, as well as in future quarters. And with the stock still not exactly cheap, there’s room for shares of Salesforce to slide further down. Even though the stock has fallen sharply of late, it’s still well above its 52-week low of $193.68.

Is Salesforce stock a buy?

Salesforce’s business isn’t broken, nor is it in bad shape. The company still grew its operations last quarter, and it did so while posting a profit. The business itself isn’t in trouble, but high expectations can put immense pressure on the company to perform at a high level — and Salesforce isn’t delivering.

That’s why this isn’t a stock I’d buy today, as there could be more losses ahead due to its high valuation. While Salesforce’s platform may be enhanced due to AI, the results aren’t there to back up management’s optimism about future growth. And until that changes, I would hold off on investing in the company, as there are better growth stocks to consider.

Should you invest $1,000 in Salesforce right now?

Before you buy stock in Salesforce, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Salesforce wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $750,197!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of June 3, 2024

David Jagielski has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Salesforce. The Motley Fool has a disclosure policy.

Is Salesforce Stock in Trouble? was originally published by The Motley Fool

From: Yahoo.com

Financial News